All Categories

Featured

Table of Contents

For most individuals, the greatest issue with the boundless financial principle is that first hit to very early liquidity created by the expenses. Although this con of unlimited banking can be lessened substantially with correct policy design, the first years will constantly be the most awful years with any Whole Life policy.

That stated, there are certain infinite banking life insurance coverage policies made mostly for high very early cash money worth (HECV) of over 90% in the first year. The long-lasting efficiency will certainly often considerably delay the best-performing Infinite Banking life insurance plans. Having accessibility to that additional 4 figures in the first few years might come at the cost of 6-figures down the roadway.

You in fact obtain some significant lasting advantages that aid you recover these early prices and after that some. We locate that this impeded early liquidity problem with unlimited financial is more psychological than anything else as soon as thoroughly discovered. As a matter of fact, if they absolutely required every penny of the cash missing out on from their limitless banking life insurance policy policy in the very first few years.

Tag: boundless banking concept In this episode, I speak about funds with Mary Jo Irmen who shows the Infinite Banking Concept. This topic may be debatable, however I wish to get varied views on the show and find out concerning different strategies for farm monetary management. Several of you might agree and others won't, but Mary Jo brings a really... With the surge of TikTok as an information-sharing platform, financial recommendations and strategies have actually located a novel means of spreading. One such approach that has actually been making the rounds is the unlimited banking idea, or IBC for brief, amassing recommendations from stars like rap artist Waka Flocka Fire. While the method is currently popular, its origins trace back to the 1980s when financial expert Nelson Nash presented it to the globe.

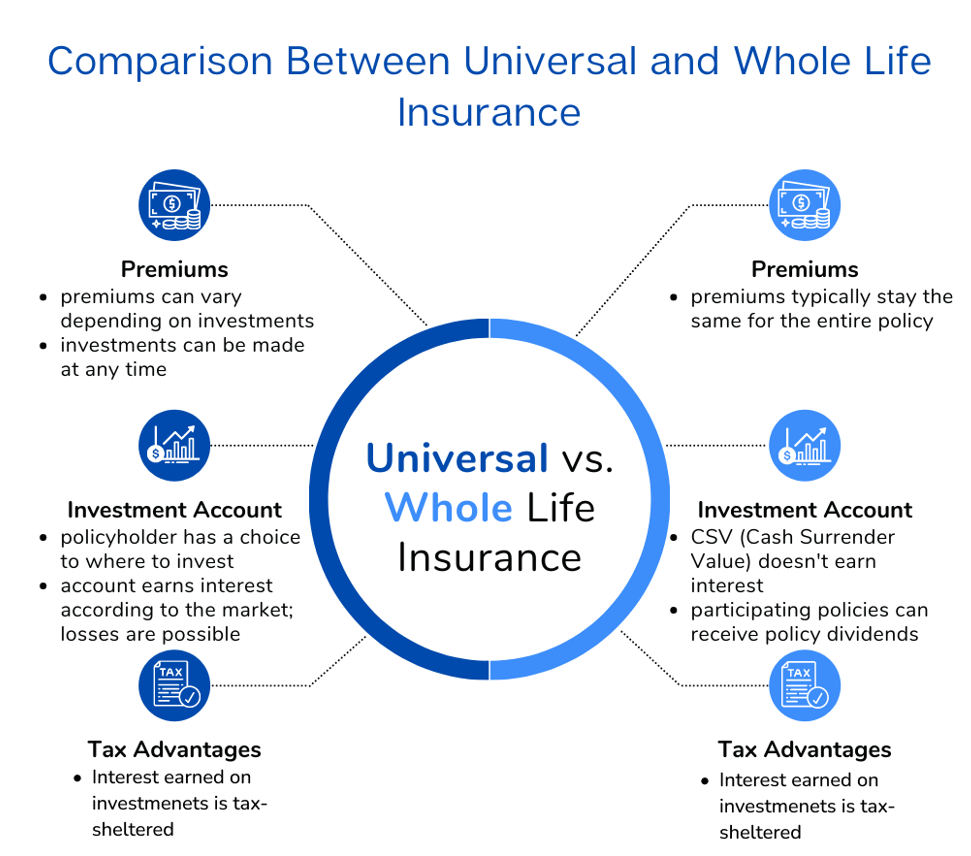

Within these plans, the money worth expands based on a price established by the insurance company. Once a significant cash money worth builds up, insurance policy holders can get a cash worth lending. These fundings differ from conventional ones, with life insurance policy working as security, suggesting one might shed their insurance coverage if loaning excessively without sufficient money value to sustain the insurance coverage expenses.

And while the attraction of these plans is apparent, there are natural limitations and dangers, requiring attentive cash money value surveillance. The technique's authenticity isn't black and white. For high-net-worth people or local business owner, specifically those making use of techniques like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance development might be appealing.

Youtube Infinite Banking

The allure of infinite banking doesn't negate its difficulties: Cost: The fundamental requirement, a long-term life insurance coverage plan, is more expensive than its term counterparts. Eligibility: Not everybody gets entire life insurance policy due to strenuous underwriting processes that can exclude those with particular health and wellness or lifestyle problems. Intricacy and danger: The elaborate nature of IBC, coupled with its dangers, may hinder several, especially when less complex and less high-risk options are readily available.

Alloting around 10% of your regular monthly income to the policy is simply not feasible for the majority of people. Making use of life insurance policy as a financial investment and liquidity source needs technique and monitoring of plan cash money worth. Seek advice from a financial consultant to figure out if unlimited financial lines up with your top priorities. Part of what you read below is simply a reiteration of what has currently been said over.

Before you obtain yourself right into a scenario you're not prepared for, recognize the adhering to first: Although the concept is commonly offered as such, you're not actually taking a car loan from on your own. If that held true, you would not have to settle it. Rather, you're obtaining from the insurer and have to settle it with rate of interest.

Some social networks blog posts suggest making use of cash worth from entire life insurance policy to pay down charge card financial debt. The concept is that when you repay the loan with passion, the amount will certainly be returned to your investments. That's not just how it works. When you pay back the funding, a portion of that interest mosts likely to the insurer.

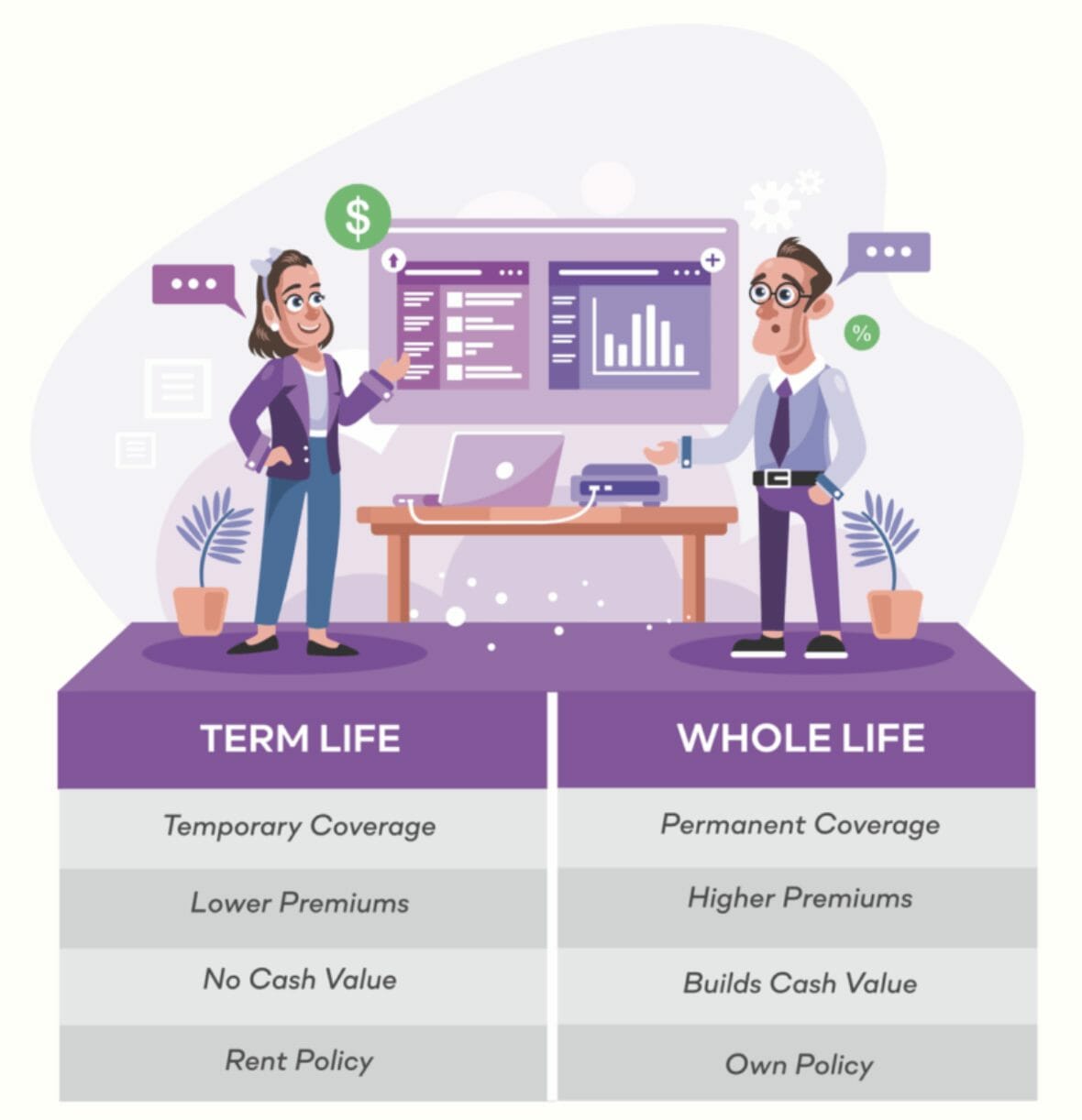

For the initial several years, you'll be settling the compensation. This makes it extremely hard for your plan to gather worth throughout this time. Whole life insurance coverage expenses 5 to 15 times a lot more than term insurance coverage. Most individuals just can not afford it. So, unless you can pay for to pay a couple of to several hundred dollars for the next decade or more, IBC will not help you.

Infinite Banking Concept Reviews

If you call for life insurance, here are some valuable ideas to consider: Think about term life insurance coverage. Make certain to go shopping around for the best rate.

Copyright (c) 2023, Intercom, Inc. () with Reserved Font Style Name "Montserrat". This Typeface Software is licensed under the SIL Open Up Font Certificate, Variation 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Typeface Name "Montserrat". This Font style Software is certified under the SIL Open Up Font License, Variation 1.1.Miss to main material

Whole Life Insurance Banking

As a certified public accountant concentrating on real estate investing, I have actually brushed shoulders with the "Infinite Financial Principle" (IBC) a lot more times than I can count. I have actually even interviewed specialists on the topic. The primary draw, other than the noticeable life insurance coverage advantages, was always the concept of accumulating money worth within a long-term life insurance coverage plan and borrowing versus it.

Sure, that makes good sense. Truthfully, I always believed that money would certainly be much better spent straight on financial investments rather than channeling it via a life insurance policy Until I found how IBC could be combined with an Irrevocable Life Insurance Coverage Trust Fund (ILIT) to produce generational riches. Let's begin with the basics.

Bank On Yourself Strategy

When you borrow against your policy's money worth, there's no set payment routine, giving you the flexibility to manage the car loan on your terms. On the other hand, the money value remains to expand based on the policy's guarantees and dividends. This setup allows you to gain access to liquidity without interfering with the long-term growth of your policy, offered that the finance and interest are handled sensibly.

The process proceeds with future generations. As grandchildren are born and grow up, the ILIT can acquire life insurance coverage policies on their lives. The count on after that gathers several policies, each with growing cash worths and survivor benefit. With these plans in position, the ILIT efficiently ends up being a "Family Bank." Member of the family can take car loans from the ILIT, making use of the money value of the plans to money investments, begin organizations, or cover major costs.

An important aspect of managing this Family Financial institution is using the HEMS criterion, which stands for "Health, Education, Upkeep, or Assistance." This standard is frequently included in trust agreements to route the trustee on exactly how they can distribute funds to recipients. By sticking to the HEMS standard, the trust makes sure that distributions are produced necessary demands and long-lasting assistance, safeguarding the depend on's properties while still supplying for family members.

Raised Versatility: Unlike stiff financial institution finances, you regulate the payment terms when obtaining from your own plan. This enables you to framework repayments in a manner that lines up with your business cash money flow. can i be my own bank. Improved Capital: By funding overhead through policy lendings, you can possibly liberate cash that would certainly or else be linked up in traditional loan settlements or devices leases

He has the very same equipment, however has likewise constructed additional cash money value in his policy and obtained tax obligation benefits. And also, he now has $50,000 readily available in his policy to utilize for future possibilities or costs., it's important to view it as even more than simply life insurance coverage.

How To Start Infinite Banking

It's concerning creating an adaptable funding system that provides you control and supplies numerous advantages. When made use of purposefully, it can match other financial investments and business approaches. If you're intrigued by the capacity of the Infinite Banking Principle for your organization, here are some actions to consider: Inform Yourself: Dive deeper right into the principle via reliable publications, workshops, or consultations with educated experts.

{kind=link}

Latest Posts

How To Train Yourself To Financial Freedom In 5 Steps

Private Banking Concepts

Non Direct Recognition Life Insurance Companies